Main events:

• Fed sets stricter monetary policy

• CNB temporarily halted interest rate cuts

• S&P 500 index appreciated over 20% in another year

Summary:

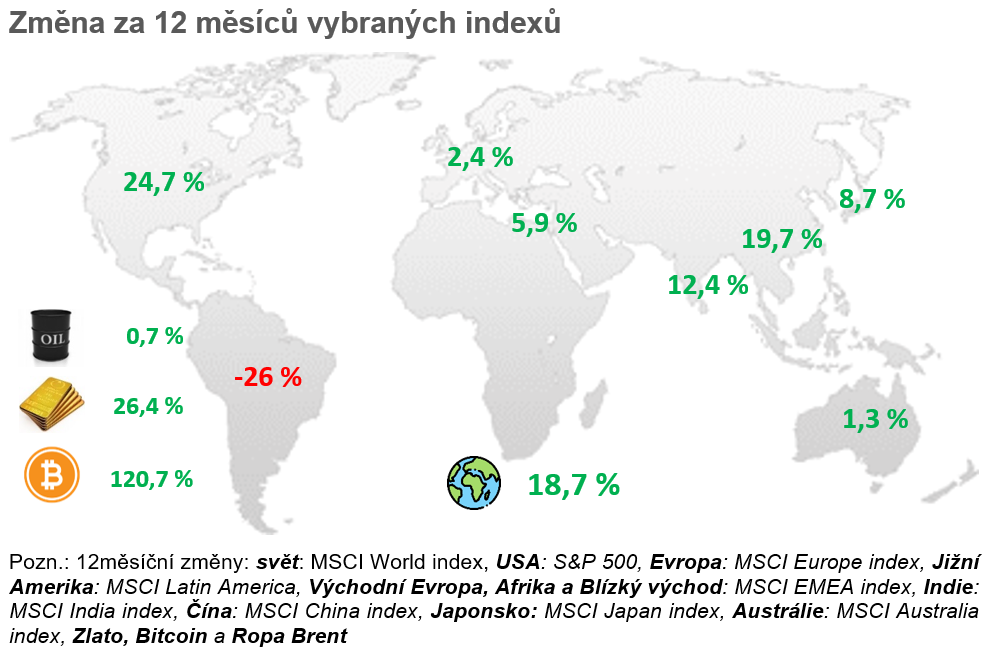

We have successfully completed the year 2024, and it could be said that almost all asset classes performed well, from stocks, bonds, to gold and bitcoin. Bond funds in the Czech Republic also performed well, but the American ones brought mixed results, and for instance, long-term government bonds even declined in price.

The American stock index S&P 500 added nearly 25% for the year 2024, continuing similar growth achieved in 2023. Along with it, the global index MSCI World performed well, and apart from Latin American countries, regions around the world brought positive results, even including China. China added 19.67% for the year 2024 (measured by the MSCI China index).

Who would have expected such positive stock growth when at the beginning of the year it was assumed that a recession was imminent, and interest rates and consequently bond yields were still at elevated levels, which should rather push stock prices down, not up.

As I mentioned, strong growth was recorded for the entire year in gold, specifically 26.44%, and especially Bitcoin, which added 120.69% for the year 2024.

But let’s move on to macroeconomic figures, where the year-on-year inflation rate in the USA came out again slightly above expectations in November at 2.7%. However, in the following months, it is expected to drop again almost to the 2% level.

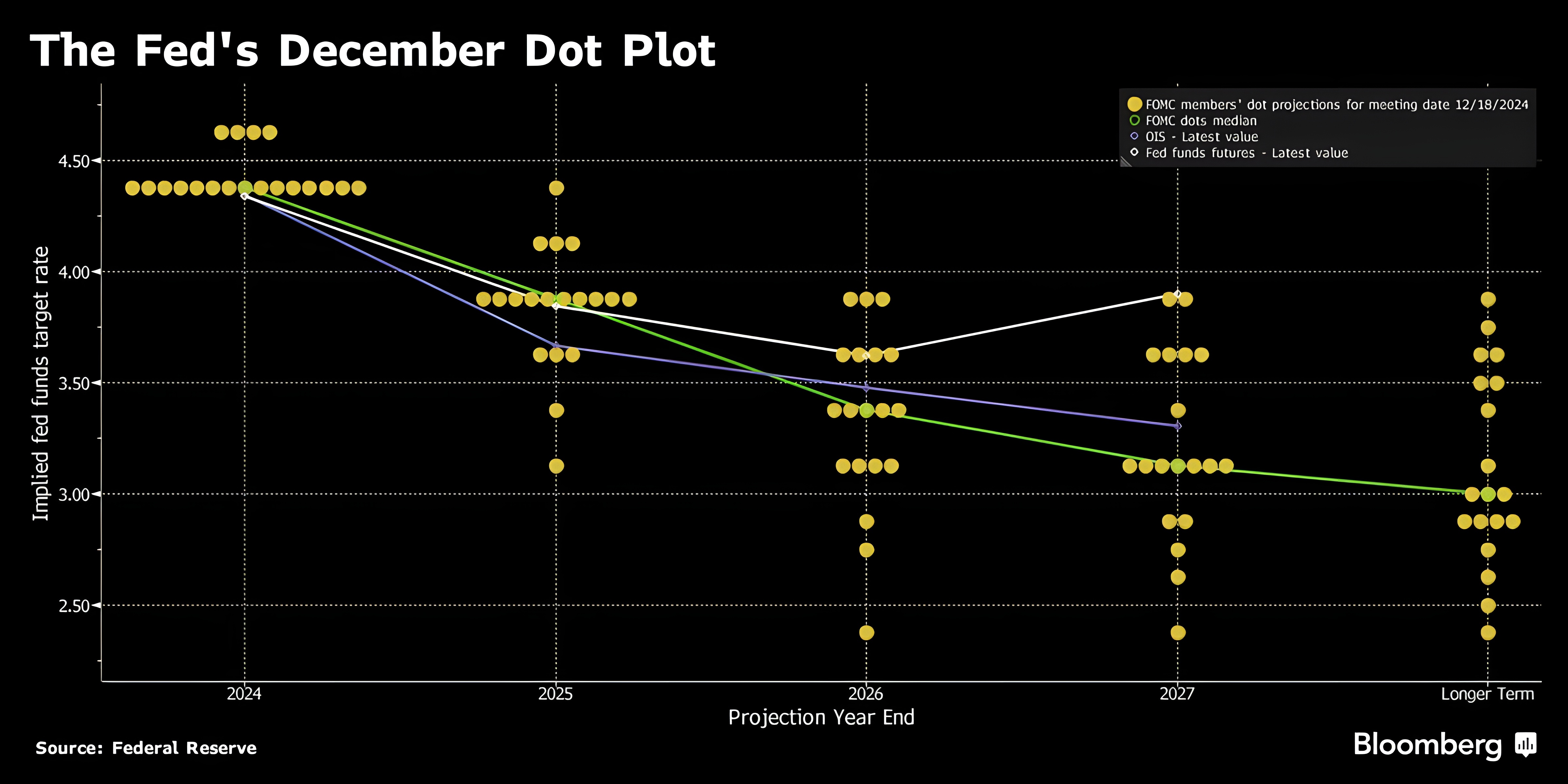

The major topic was the Fed meeting held on 18.12. 2024. At this meeting, there was a gradual expected reduction in the interest rate from 4.75 to 4.5%, but future predictions regarding reductions surprised investors.

Further stricter monetary policy settings and only a slight reduction in interest rates to 4% for 2025 are expected. As a result, yields on medium and long-term US government bonds rose, and stocks fell by 3 to 4% (S&P 500) in a single day.

The year-on-year inflation rate for November in the Czech Republic again came out at an elevated level of 2.8%. The repeated increase was due to more expensive food, and in the short term, the year-on-year inflation rate is expected to rise to the 3% threshold.

The CNB, at its meeting on 19.12. 2024, for the first time in a long time, left interest rates unchanged at the level of 4%.

As for year-on-year inflation results in Europe, it came out at 2.2% for November. However, a slight increase to 2.4% is expected in the coming months.

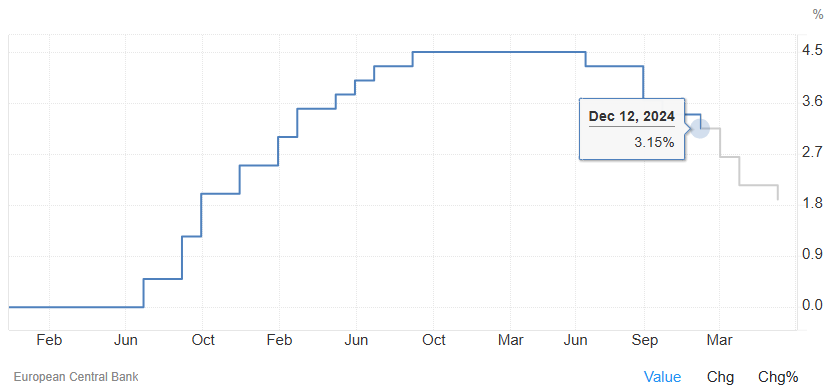

The ECB continues to reduce interest rates, which it reduced from 3.4 to 3.15%. Unlike the Fed, it plans to continue reducing them to 2%, which it expects for the end of 2025.

Czech Republic:

The year-on-year inflation rate for November in the Czech Republic again came out at an elevated level of 2.8%. The repeated increase was due to more expensive food, and in the short term, the year-on-year inflation rate is expected to rise to the 3% threshold.

The CNB continues to expect a slight increase in inflation due to rising goods prices and a low base from the previous year. The growth in service prices remains elevated, reflecting rapid wage growth.

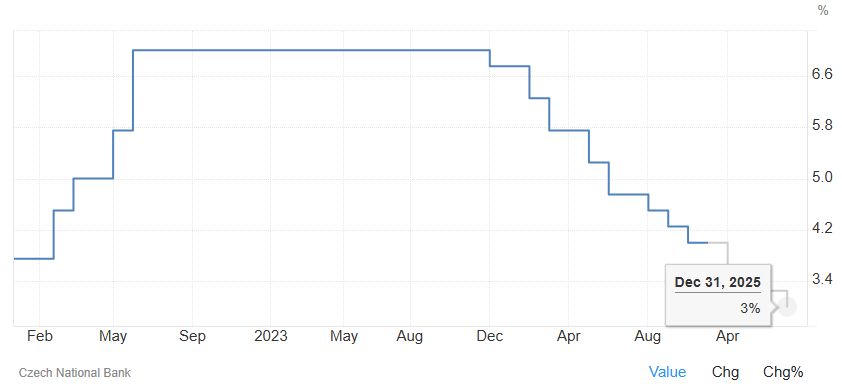

As a result, the CNB at its last meeting on 19.12. 2024, left interest rates at the level of 4%. Five out of seven members voted for keeping the rates unchanged. The remaining voted for a reduction to 3.75%.

Expectations of interest rate cuts in the Czech Republic

Source: tradingeconomics.com

The CNB will proceed cautiously with further interest rate cuts, evaluating based on new data. Currently, it expects a gradual reduction to 3% by the end of 2025.

USA:

The year-on-year inflation rate in the USA came out again slightly above expectations in November at 2.7%. However, in the following months, it is expected to drop again almost to the 2% level.

The major topic was the Fed meeting held on 18.12. 2024. At this meeting, there was a gradual expected reduction in the interest rate from 4.75 to 4.5%, but future predictions regarding reductions surprised investors.

Fed’s forecast regarding interest rate cuts in the USA

Source: Bloomberg

Further stricter monetary policy settings and only a slight reduction in interest rates to 4% for 2025 are expected. As a result, yields on medium and long-term US government bonds rose, and stocks fell by 3 to 4% (S&P 500) in a single day.

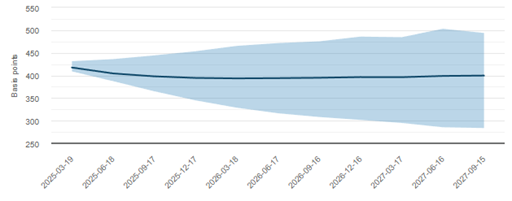

Investors’ expectations regarding interest rate cuts in the USA

Source: AtlantaFed

Investors and the bond market thus signal that the Fed will only proceed with two more interest rate cuts by the end of the year, and in the long term, will hold the rate at 4%. This is certainly a higher level than was expected just a few months ago.

US GDP continues to grow, inflation is under control, and unemployment remains at a stable level. At the same time, under Trump, higher government deficits are expected, and for these reasons, the Fed’s policy will be stricter.

The S&P 500 index slightly declined by 2.41% in December. For the entire year, the index added 24.69% and the technology index NASDAQ 100 grew similarly, specifically 25.32%.

Europe:

The year-on-year inflation rate in Europe for November came out at 2.2%. However, a slight increase to 2.4% is expected in the coming months.

The ECB continues to reduce interest rates, which it reduced from 3.4 to 3.15% in December. Unlike the Fed, it plans to continue reducing them to 2%, which it expects for the end of 2025.

The ECB continues to reduce interest rates

Source: tradingeconomics.com

Unlike the Fed, the ECB wants to further support the economy and GDP growth. Especially the economy in Germany, where we still do not see an improvement in their situation.

European stocks added only 2.4% for the entire year in dollar terms. In the domestic currency, the euro, Europe achieved a return of 8.87% for the year 2024. Nevertheless, American stocks added a higher overall return.

Surprisingly, the highest return was achieved by the German DAX index, specifically 18% for the year 2024. This is because a larger part of the index is linked to the financial and technological sector, which drove the German index up.