Financial Market Commentary – October 2022

Highlights:

- High inflation

- Decline in energy prices

- China’s economy in trouble

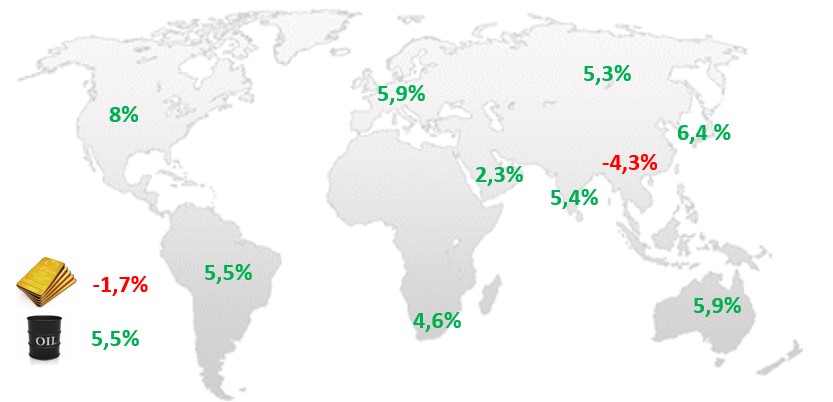

Changes in selected stock indices and commodities:

Commentary:

The S&P 500 gained 8% in October as more than half of U.S. companies reported Q3 results. Of those, 72% beat expectations, with the long-term average being 66%. In Western Europe (+6.3%), 58% of results surprised positively, but here only 53% surprise on average and less than a third of companies have reported so far. In the US, energy and industrial stocks rose the most, while in Europe the travel sector led the way. US Q3 GDP confirmed the recovery from the technical recession. Central European equities (+11%) lifted their historically low valuations, but the Prague Stock Exchange (+5.4%) lagged, partly due to the debate on taxes on extraordinary gains. Government bond prices continued to fall in October, and mainly in the US, Germany and Central Europe in particular. In the case of the Czech market, the increase in bets on a possible CNB interest rate hike had an impact. The Chinese economy continues to languish due to a slump in the property segment, covid lockdowns and weak demand for Chinese exports. Investors were also little pleased with the results of a key party congress, where President Xi Jinping installed supporters of government intervention and a “zero tolerance” policy towards covid loyal to him in key positions. In addition, the US has moved to further tighten Chinese firms’ access to US technology, specifically chips.

US:

The Fed continues to tighten monetary policy due to high inflation. The real economy returned to growth in the third quarter from the technical recession of the first half of the year, when it grew at an annualized rate of 2.6%. Growth was mainly driven by net exports followed by domestic demand. The unemployment rate fell to 3.5% in September from 3.7% in August. Rapid job creation also continued, with the US economy creating 1 million new private sector jobs in July-September. Durable goods orders rose month-on-month at the end of the third quarter. In addition, industrial production continues to perform well. It rose by 0.4% in real terms in September to an annualised real growth rate of 5.3%. At the meeting in early November, the Fed raised rates again by three-quarters of a percentage point to 3.75%-4.00%, although the Fed reiterated its message from the previous two meetings that it would move at a slower pace in the future and that a slowdown in the pace of rate increases would likely occur at one of the next two meetings. At a press conference in early November, Fed President Powell ruled out a stop to rate tightening. He indicated that the Fed would have to raise interest rates to a higher level than the 4.50%-4.75% indicated in September. In response, investors raised expectations of a rate peak at 5.00-5.25% and said “the economy will need a long period of low growth and higher unemployment to tame inflation”, adding that he wants to see positive real interest rates across the curve.

EU:

Inflation accelerates further, outlook for industry and services deteriorates further. However, neither the labour market nor economic growth confirm the concerns so far. The first estimate of the GDP growth rate in Q3 was again better than expected. In fact, the growth rate remained positive. Of the major economies, Italy fared the best, followed by Germany, with Spain and France close behind. Retail sales fell again in the middle of the third quarter, for the third consecutive quarter. After falling by 1% in June and 0.4% in July, they fell by 0.3% in August. However, the first data for some countries for September show an improvement. The fact that sales continue to do relatively well is of course due to the fact that the labour market is still in excellent shape. The seasonally adjusted unemployment rate is down by 1 pp yoy and remains below 7%. Unemployment is lowest in Germany (3%) and highest in Spain (12.4%). Wage growth remains relatively subdued. According to the data, the scenario of inflation spilling over into wages is not yet materialising. However, we are seeing the first signs that wages will accelerate in the form of strikes and bargaining at large companies. Industrial production, after a surprisingly strong second quarter, declined in the first two months of Q3, albeit only slightly in aggregate. In fact, it lost 2.3% month-on-month in July, but rose by 1.5% month-on-month in August. The annual growth rate of total industrial production was +1.5% in the middle of the third quarter, and even +1.7% in the manufacturing sector. This is a very surprising result in the light of the energy crisis and inflation and does not correspond to the pessimism repeatedly expressed by firms in surveys. This pessimism is also evident in the October surveys. The manufacturing Purchasing Managers’ Index (PMI) deteriorated further in October 2022: from 48.4 points in September, it fell to its lowest level in 29 months, i.e. 46.6 points. The worst performer was Germany, where the index fell to 44.1 points, the weakest result since June 2009, excluding the pandemic. The reason for the decline (not only in Germany) was the drop in new orders, which was the largest since April 2009. In the dominant service sector, the situation in the euro area also deteriorated further in October, mainly due to a fall in new orders, which fell at the highest rate (excluding the pandemic) since June 2013. According to preliminary data, inflation accelerated to 10.7% yoy in October with its 1.5% month-on-month growth. Tracked core inflation accelerated by 0.6% m-o-m, taking it from September’s 4.8% y-o-y to October’s 5%. Among the major countries, inflation in September was highest in Germany (11.6%) and Italy (12.8%), and lowest in France (7.1%) and Spain (7.3%). The first September data from Germany or Italy suggest that producer price inflation was not over in the euro area even in September. The ECB has sent cautious signals that it will not be as hot with further rate hikes as it might have seemed a few months ago. While it did raise rates again in October by 0.75ppt to the highest level since 2009 and said it “must do what is necessary” to tame inflation, it also changed its outlook from “rates will rise at the next few meetings”, which was the sentence in the September minutes, to “we expect rates to rise further” in October. The markets interpreted this to mean that a peak and perhaps even a reversal in rates was imminent. However, inflation, the labor market, and other data do not support any such thing. Core inflation in the euro area is still very high.

CR:

The economy is showing the first signs of cooling, but neither the labour market nor core inflation is much affected yet. According to the first data, GDP growth in Q3 was -0.4% q-o-q, which meant a positive pace of +1.6% y-o-y. Structural data have not yet been published, but according to the Czech Statistical Office, the quarter-on-quarter decline was mainly due to weaker household demand. In contrast, foreign demand had a positive effect. Monthly data published during October 2022 were weak, with the exception of industry. Industrial production rose again in August 2022. After strong growth in May and June (+2% and +1.8% m/m), it fell by 0.2% m/m in July but added 0.8% m/m in August. Its y/y pace thus came in at +7.2%, the best y/y result since July 2021. Automotive, electrical equipment and other machinery production contributed the most to the y/y growth rate. The fact that the situation in industry is not (yet) catastrophic is shown by the fact that the number of employees has de facto stagnated year-on-year (employment -0.1% yoy). However, the development of the PMI index does not correspond much with this description of the situation. This index has continued to fall after breaking below the 50-point mark in June (for the first time since August 2020). In September it fell to 44.7 points and in October it even fell to 41.7 points, the lowest since May 2020. The reason for the decline was both a fall in existing production (the fastest since May 2020) and a fall in new orders (the fastest since April 2020). However, prices of inputs and outputs continued to rise, albeit in both cases at a slower pace than in previous months. The (September) CSO survey of business confidence also looks negative, with confidence in October falling to its lowest level (5.0 points) since March 2021. The situation is even worse for households, and is in line with what one would expect in a high inflation situation – their confidence is falling, with a new all-time low in October. The trend in retail sales is beginning to match the pessimism – in the three months to August, sales have fallen by 2.6% in real terms, with a decline of 5.2% in the last 6 months. At the same time, sales can be expected to continue to weaken.

At the CNB meeting at the beginning of November, rates remained stable at 7%. The newly presented autumn forecast does not differ much from the summer forecast in terms of the inflation outcome for next year – while the summer forecast expected average inflation of 9.5%, the new autumn forecast sees it at 9.1%. However, the way in which the Czech economy is expected to reach the same outcome differs. The new way is more painful. While in the summer the CNB claimed that rates would fall next year (average PRIBOR in 2023 was expected to be around 5%) and the economy would avoid recession (GDP growth was expected to be positive 1.1%), today everything is different. The CNB expects average PRIBOR to be 7% in 2023 (and even 5% in 2024) and the economy to contract by less than a percent next year. Add to this the expectation of a strongly